Shanghai, China – March 20, 2026 – Chinese equity markets experienced a slight uptick today, buoyed by the People’s Bank of China’s decision to maintain its key lending rates unchanged for the tenth consecutive month. This stability in monetary policy provided a sense of relief to investors, contributing to modest gains in the Shanghai Composite Index and the Shenzhen Component Index. Meanwhile, the U.S. dollar saw a notable strengthening against major currencies, including the Japanese Yen and the Euro, while oil prices experienced a dip amidst developments from the European Union and Japan.

The Shanghai Composite Index closed trading up by 0.2%, reaching 4,013.16 points. The broader index encompassing major stocks from Shanghai and Shenzhen rose by 1.0%, settling at 4,626.90 points. This positive performance reflects investor confidence in the continued accommodative stance of Chinese monetary policy, which aims to support economic recovery without triggering inflationary pressures.

Background: China’s Monetary Policy Landscape

The People’s Bank of China (PBOC) has been navigating a complex economic environment, balancing the need for growth stimulation with concerns over inflation and currency stability. In recent months, the central bank has signaled a cautious approach, preferring to hold benchmark interest rates steady rather than implementing aggressive rate cuts. This strategy is partly influenced by global economic uncertainties, including geopolitical tensions and fluctuations in commodity prices.

The decision to keep the Loan Prime Rate (LPR) unchanged – at 3.0% for the one-year tenor and 3.5% for the five-year tenor – aligns with market expectations. Analysts have pointed to several factors influencing this decision. Firstly, the lingering effects of the Middle East conflict have contributed to elevated oil prices, a key driver of inflation. This has diminished the immediate urgency for further monetary easing, as such measures could exacerbate inflationary risks. Secondly, surprisingly robust economic data from China for January and February provided further justification for a steady hand at the PBOC. These figures indicated a resilient domestic economy, reducing the perceived need for drastic stimulus measures.

Asian Markets React to Unchanged Rates and Global Developments

Beyond China, the MSCI Index for Asian equities, excluding Japan, recorded a marginal increase of 0.18%. This broad-based movement suggests that the stability in China’s interest rates offered a positive signal across the region. However, the markets were also influenced by other significant global events.

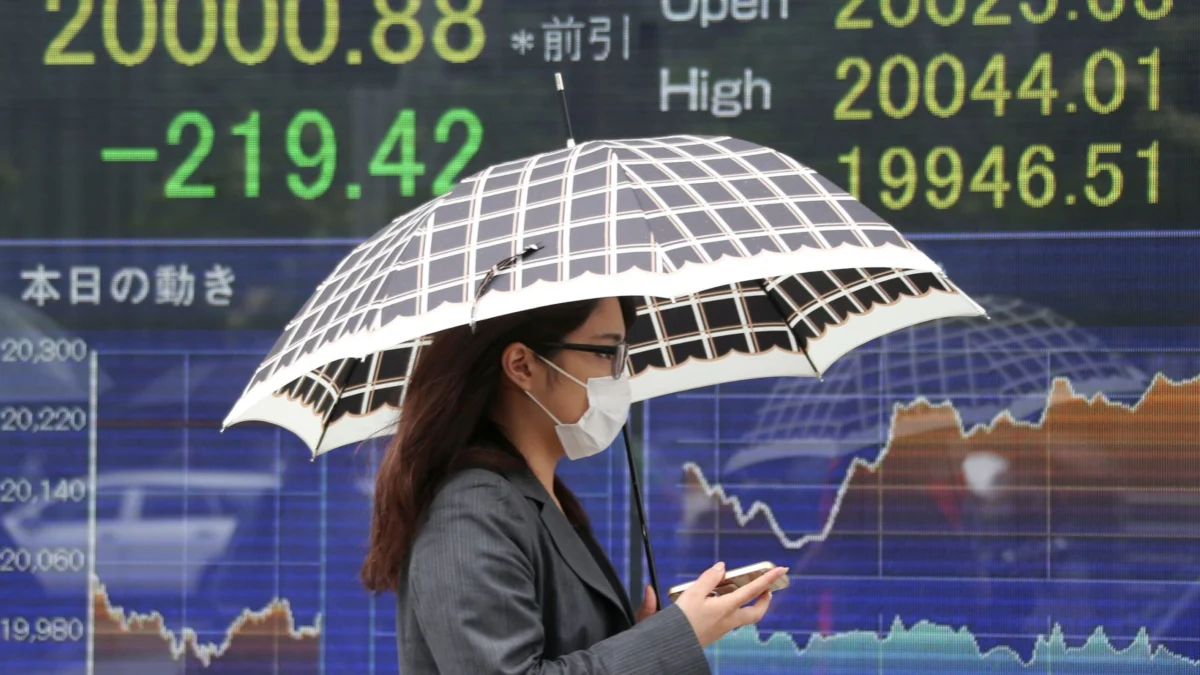

The Tokyo Stock Exchange remained closed today, a routine occurrence for Japanese financial markets. This closure meant that Japanese market sentiment and its potential impact on regional trading were deferred.

U.S. Dollar Gains Momentum Amidst Global Uncertainty

In the foreign exchange markets, the U.S. dollar demonstrated considerable strength. It appreciated by 0.4% against the Japanese Yen, reaching 158.30 Yen. The dollar also saw a modest gain against the Chinese Yuan, trading at 6.8942 Yuan. This surge in the dollar’s value is attributed to its status as a safe-haven asset during periods of global instability. Investors tend to flock to the dollar when geopolitical risks are high, seeking refuge in its perceived stability and liquidity. Furthermore, the United States’ position as a significant energy exporter may also be contributing to the dollar’s strength, particularly as oil prices remain a point of concern for global inflation.

Euro Faces Downward Pressure

The Euro experienced a decline in Asian trading, falling by 0.3% to 1.1558 U.S. dollars. This weakening of the Euro can be linked to a confluence of factors, including the strengthening dollar and potential concerns stemming from economic outlooks within the European Union. While specific EU-related news was not detailed in the initial report, broader market sentiment often reacts to economic indicators and policy pronouncements from major economic blocs. The Euro’s dip suggests that investors are favoring the U.S. dollar as a more secure investment in the current global climate.

Oil Prices Exhibit Volatility

While the initial report mentioned oil prices as a factor influencing China’s monetary policy, the specific price movement on this particular trading day was a decline. This could be attributed to a variety of factors, including shifts in supply expectations, inventory data, or broader market sentiment regarding global demand. The dynamic nature of oil prices, heavily influenced by geopolitical events and economic forecasts, continues to be a key indicator for inflationary trends and global economic health.

Analysis of Implications

China’s decision to maintain interest rates provides a stable footing for its domestic economy, offering predictability for businesses and consumers. This approach suggests a confidence in the ongoing recovery and a desire to avoid overheating the economy. For equity markets, this stability is generally positive, reducing uncertainty and encouraging investment.

The strengthening U.S. dollar has dual implications. For the U.S. economy, it can make exports more expensive but imports cheaper, potentially influencing trade balances. Globally, a strong dollar can pose challenges for countries with dollar-denominated debt, increasing their repayment burdens. It also impacts commodity prices, as many are priced in dollars.

The decline in the Euro, while modest, indicates a preference for dollar-denominated assets. This trend could persist as long as global uncertainties remain elevated. The interplay between these currency movements and commodity prices, particularly oil, will be closely watched by policymakers and investors alike in the coming weeks and months.

Looking Ahead

The coming days will likely see continued attention paid to economic data releases from major global economies, as well as any further developments on the geopolitical front. The PBOC’s next move on interest rates will be a key indicator of its assessment of China’s economic trajectory, while the performance of the U.S. dollar will offer insights into global risk sentiment. The resilience of Asian equity markets, particularly in the context of Japan’s market reopening, will also be a significant factor to monitor. The delicate balance between managing inflation, supporting growth, and navigating international economic headwinds will continue to shape financial market dynamics.