The widespread perception of stablecoins as straightforward digital representations of fiat currency, primarily the U.S. dollar, belies a complex and increasingly fragmented market structure. While designed to offer stability in the volatile cryptocurrency landscape, the reality of moving and trading these assets on-chain often mirrors a disjointed foreign exchange market, where liquidity is dispersed across numerous blockchains, issuers, and decentralized finance (DeFi) venues. This fragmentation leads to significant price differences, uneven access to dollar liquidity, and a challenging user experience, particularly as institutional players increasingly enter the digital asset space.

At its core, the issue stems from stablecoins not behaving as a unified asset class. A stablecoin pegged to the dollar on one blockchain may not be directly fungible or equivalent to the "same" stablecoin on another chain or even within a different liquidity pool on the same chain. This creates a labyrinthine environment where what appears to be a simple transfer of value from point A to point B often involves multi-step transactions routed across disparate ecosystems. Ryne Saxe, CEO of stablecoin infrastructure company Eco, aptly described this phenomenon to Cointelegraph: "It’s a very special case of a foreign exchange market onchain, and that leads to bad user experience, with unexpected slippage, transaction reversion and unfamiliar information when moving your dollar from point A to point B."

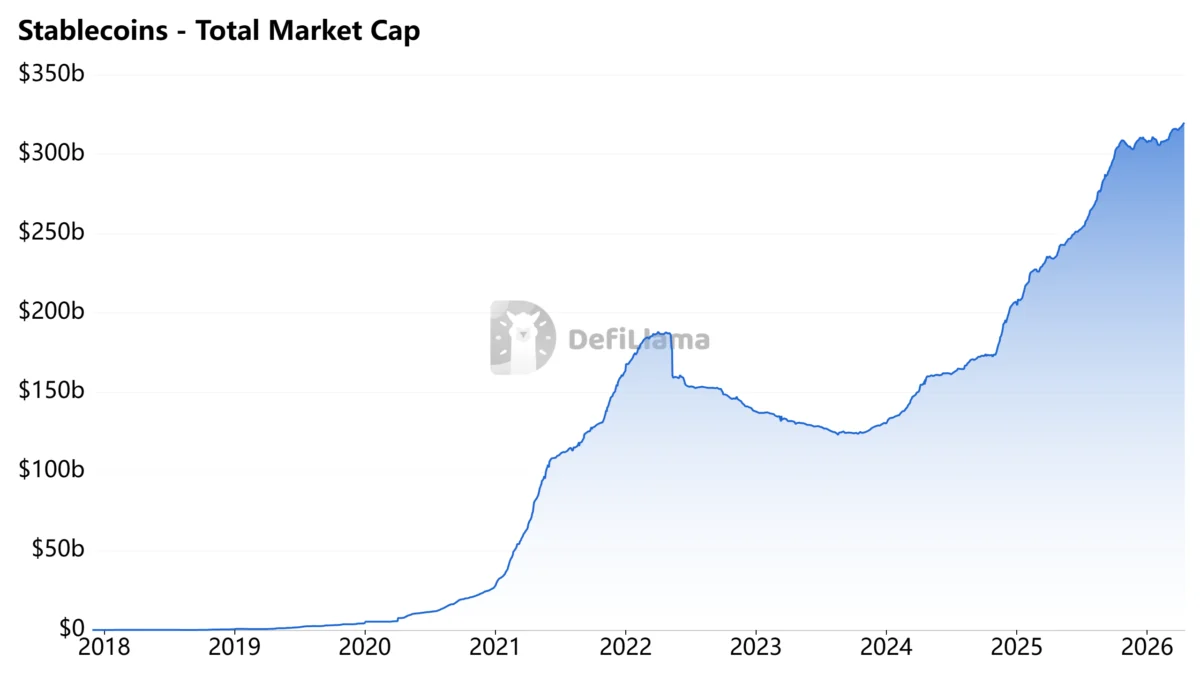

The stablecoin market has witnessed phenomenal growth, with a cumulative market capitalization now exceeding $320 billion. This expansion is largely spearheaded by giants like Tether’s USDt (USDT) and Circle’s USDC (USDC), which collectively command the lion’s share of the market. Their ubiquity across various blockchain networks underscores their critical role in the broader crypto economy, serving as primary conduits for trading, collateralization, and cross-border settlements. However, this very success, coupled with the multichain paradigm of Web3, has inadvertently exacerbated the fragmentation challenge. As the market matures and larger traders and institutions seek to deploy significant capital, the inherent complexities of stablecoin movements become increasingly pronounced, demanding robust and efficient solutions.

The Illusion of Fungibility: Deconstructing Stablecoin Disparity

The promise of stablecoins was simple: a digital asset whose value is pegged to a stable asset, typically a fiat currency like the U.S. dollar. This peg is meant to ensure that 1 stablecoin always equals 1 unit of the underlying currency. However, the operational reality deviates significantly from this ideal. Stablecoins, while pegged, do not trade as a singular, unified asset. Instead, their liquidity is splintered across multiple issuers, a multitude of blockchains, and countless decentralized finance (DeFi) venues. Each of these segments possesses its own unique depth, pricing mechanisms, and access conditions, creating a patchwork of dollar liquidity rather than a cohesive whole.

"Stablecoins, between them, aren’t very fungible," Saxe emphasized, highlighting the fundamental challenge. The differing profiles across these numerous markets mean that achieving seamless and efficient pricing and movement of stablecoins is a far more complex undertaking than most users or even some market participants assume. This complexity arises from several factors, including variations in collateral backing, regulatory compliance standards of issuers, and the sheer depth of liquidity available in specific pools or on particular chains. These differences, often subtle, can create noticeable pricing gaps that widen considerably with larger transaction sizes or in less liquid market conditions. While negligible for small, everyday transactions, these discrepancies become critical for institutional players moving millions of dollars.

A report published in March by payments startup Borderless provided compelling data supporting this fragmented reality. Their research found that pricing divergence in stablecoins is heavily dependent on the source of liquidity. The report meticulously collected hourly buy and sell rates throughout February across 66 stablecoin-to-fiat corridors, encompassing 33 currencies and seven distinct blockchains. While the study observed that USDC and USDT generally traded at near-identical prices in the vast majority of cases – with 91% of pairs exhibiting a divergence of less than 10 basis points – significant variations emerged at the provider level. Here, pricing gaps within the same corridor could, alarmingly, exceed hundreds of basis points. This finding underscores that the quality of execution for stablecoin transactions is critically dependent on a user’s or institution’s access to optimal liquidity and their ability to effectively route transactions across various venues and providers.

The Evolution of Stablecoins and the Growth of Fragmentation

The journey of stablecoins began with a clear objective: to bridge the volatile world of cryptocurrencies with the stability of fiat currencies. Tether (USDT), launched in 2014, pioneered the concept, initially running on the Omni Layer before expanding to Ethereum and other chains. Circle’s USDC followed in 2018, aiming for greater regulatory transparency and broader institutional appeal. These early stablecoins primarily resided on a single blockchain, typically Ethereum, where the vast majority of DeFi activity was concentrated.

However, the rapid proliferation of new Layer 1 blockchains (like Solana, Avalanche, Tron, BNB Chain) and Layer 2 scaling solutions (such as Polygon, Arbitrum, Optimism) dramatically altered the landscape. Each new network sought to attract stablecoin liquidity to power its nascent DeFi ecosystem. This led to a multichain stablecoin reality, where native stablecoins were issued on some chains, while others relied on wrapped or bridged versions of existing stablecoins. For instance, a USDC on Ethereum is technically distinct from a USDC on Solana or Polygon, even though they are all backed by Circle. These bridged versions introduce additional layers of smart contract risk and technical complexity.

This multichain expansion, while fostering innovation and expanding access, has directly contributed to the current fragmentation. Instead of a single, deep pool of dollar liquidity, the market now contends with dozens of smaller, often isolated pools. Each blockchain hosts its own decentralized exchanges (DEXs) and lending protocols, each with varying levels of stablecoin liquidity. This distributed liquidity, coupled with the challenges of cross-chain communication and asset transfer, forms the bedrock of the "fragmented FX market" analogy. The growth of stablecoin market capitalization, while impressive, has outpaced the development of truly unified and efficient cross-chain liquidity infrastructure.

Institutional Hurdles: Moving Millions in a Fragmented Market

The increasing involvement of institutions in digital assets marks a significant shift for the crypto industry. These sophisticated players utilize stablecoins for a multitude of purposes, including high-volume trading, efficient cross-border payments, and strategic on-chain treasury management. For institutions, stablecoins are crucial for transferring capital between exchanges and protocols, settling large trades, and tapping into the yield opportunities prevalent across DeFi markets. Unlike retail users, who typically transact smaller amounts, institutions often need to move tens of millions, if not hundreds of millions, of dollars at a time. For these operations, execution must be swift, predictable, and highly efficient, with minimal slippage and robust risk management.

It is precisely at this scale that the current market fragmentation becomes a critical impediment. As Saxe explains, "If liquidity is spread out, trying to sell $10 million of one stablecoin and buy $10 million of another in a single step will move the market." This market impact, often resulting in significant slippage, translates directly into higher costs and reduced capital efficiency for institutions. To mitigate this, traders are often forced to break down large transactions into multiple, smaller branches, which may be routed differently across various chains and liquidity pools before converging at the final destination. This multi-step process introduces considerable operational complexity, increases transaction fees, and, crucially, adds uncertainty to the execution outcome.

The challenge is not merely about finding a stablecoin, but about finding sufficient depth of liquidity for a specific stablecoin on a specific chain at a specific time. Instead of drawing from a single, deep global pool of dollar liquidity, institutions must navigate a complex ecosystem of numerous chains, various stablecoin issuers, and countless DeFi venues, each with its own distinct liquidity conditions. This intricate navigation, especially when moving substantial sums, can trigger price shifts, necessitate sophisticated trade splitting algorithms, and introduce a level of unpredictability that is unacceptable for professional financial operations. "Right now, they don’t have the risk management, trust and infrastructure that they need to move or hold a lot of stablecoins at size onchain by default," Saxe elaborated, pointing to a fundamental gap in the existing digital asset infrastructure.

Industry Responses: Building Bridges and Aggregating Liquidity

Recognizing these significant challenges, various companies and protocols are actively developing solutions, though often from different conceptual frameworks regarding the core problem. The consensus, however, points to the urgent need for enhanced infrastructure rather than merely increasing the supply of stablecoins.

One prominent approach is exemplified by Circle, the issuer of USDC. Through initiatives like Circle StableFX and Circle Partner Stablecoins, the company is positioning stablecoins as the foundational layer for a new global foreign exchange system. Their vision involves connecting multiple fiat currencies, diverse liquidity providers, and various settlement layers through a shared, interconnected infrastructure. This strategy aims to create a more unified environment where different currencies and stablecoin types can be seamlessly exchanged, reducing the friction caused by disparate systems.

Eco, on the other hand, with its CEO Ryne Saxe, focuses intently on routing and execution. Their solution involves aggregating liquidity across the highly fragmented stablecoin markets. This means developing sophisticated algorithms and protocols that can "read across markets," identify the optimal liquidity sources, and intelligently route transactions to ensure the best possible execution price and minimal slippage. This approach acknowledges the inherent fragmentation and seeks to build a layer of abstraction that shields users from its underlying complexity.

Beyond these specific company initiatives, the broader industry is witnessing a surge in cross-chain bridging solutions and liquidity aggregators. Protocols like LayerZero, Wormhole, and various intent-based architectures are striving to facilitate the seamless movement of assets and information between disparate blockchains. While these technologies promise to enhance interoperability, the challenge remains to create a truly unified liquidity experience where a dollar stablecoin on one chain can be effortlessly swapped for its equivalent on another without significant price discrepancies or technical hurdles. The goal is to evolve beyond simple asset transfers to genuine cross-chain fungibility and efficient capital allocation.

The central thesis emerging from these varied approaches is clear: the issue is not a lack of stablecoin supply, but rather the distributed and uneven nature of the liquidity backing them. Moving funds necessitates interacting with this fragmented liquidity, which inherently introduces pricing differences, routing complexities, and elevated execution risk. For institutions, this complexity directly limits the amount of capital that can predictably and safely move on-chain. As Saxe succinctly puts it, "Fragmentation creates more spread between prices, meaning worse execution in many cases. To solve that, you need to read across markets, see the full liquidity picture, even if it’s fragmented, and route across it." Until stablecoin flows achieve a far greater degree of predictability, institutions will remain hesitant to move or hold substantial amounts of capital on-chain due to the current limitations in risk management and trust infrastructure.

Broader Implications and the Path Forward

The fragmentation of stablecoin liquidity carries significant implications across the entire digital asset ecosystem. For the DeFi sector, it directly impacts capital efficiency, making it harder for protocols to access deep, unified liquidity pools for lending, borrowing, and trading. This can lead to suboptimal yield opportunities and increased risk for participants. The difficulty in efficiently arbitraging price differences across chains also means that market inefficiencies can persist longer, preventing true price discovery and market equilibrium.

For the broader adoption of digital assets by mainstream finance, addressing stablecoin fragmentation is paramount. Traditional financial institutions operate within highly regulated environments that demand predictability, transparency, and robust risk controls. The current state of stablecoin liquidity, with its inherent slippage, execution uncertainty, and multichain complexities, presents a formidable barrier. To attract and retain institutional capital, the digital asset space must evolve to offer a stablecoin experience that rivals the efficiency and fungibility of traditional fiat currency markets, but with the added benefits of blockchain technology.

Moreover, the fragmented nature of stablecoins could also pose challenges for future regulatory frameworks. As governments worldwide grapple with how to regulate stablecoins, the existence of numerous versions of the "same" stablecoin across different chains, potentially with varying collateralization standards and regulatory oversight, complicates the task of ensuring consumer protection, financial stability, and anti-money laundering compliance. A unified understanding and treatment of stablecoin liquidity will be crucial for effective regulation.

Looking ahead, the industry’s focus must shift from merely issuing more stablecoins to developing the foundational infrastructure necessary for their seamless and efficient operation across diverse networks. This will likely involve a combination of advanced cross-chain bridging solutions, sophisticated liquidity aggregation protocols, and perhaps even a move towards more standardized stablecoin issuance and interoperability layers. The ultimate goal is to transform the current fragmented stablecoin landscape into a truly unified and globally accessible on-chain dollar (or other fiat currency) liquidity market. This evolution is not just a technical challenge but a critical step towards realizing the full potential of digital assets as a foundational layer for a new global financial system, capable of serving both retail users and the demanding requirements of institutional capital. The journey from a simple on-chain dollar proxy to a truly fungible, efficient, and predictable global digital currency is ongoing, and its success hinges on overcoming the complexities of its current fragmented reality.