The signal came in the form of a succinct yet impactful message from Saylor on Sunday, when he shared a chart detailing MicroStrategy’s extensive BTC purchase history accompanied by the directive, "Think bigger." This phrase has become a recognizable harbinger for market observers, often preceding official announcements of significant Bitcoin acquisitions by the enterprise software and business intelligence firm. MicroStrategy’s aggressive and persistent accumulation strategy has positioned it as the largest corporate holder of Bitcoin globally, a stance maintained through various market cycles, including periods of significant volatility and unrealized losses.

MicroStrategy’s Unwavering Accumulation Strategy

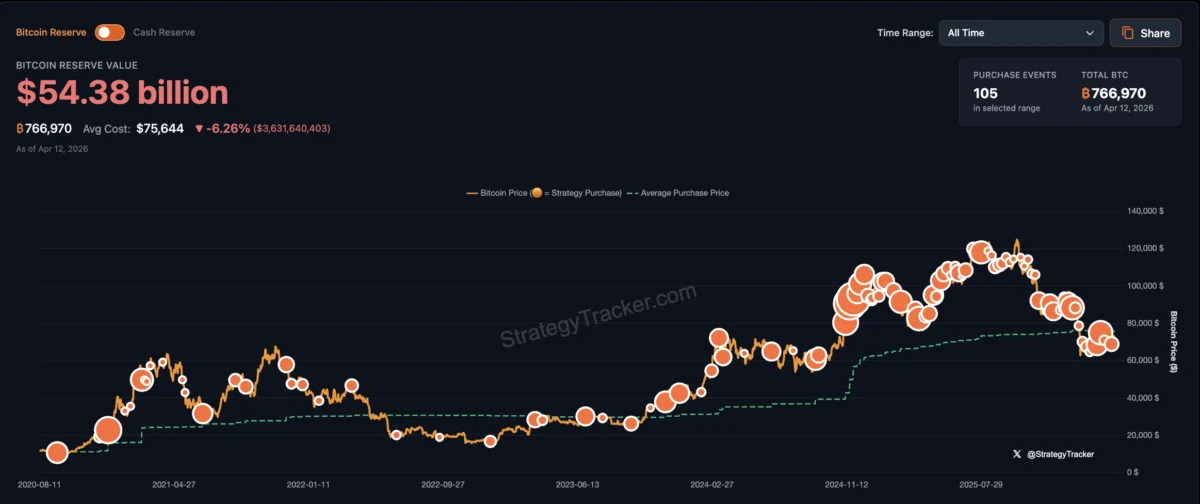

MicroStrategy’s most recent publicly disclosed Bitcoin purchase occurred on April 6, when the company added 4,871 BTC to its treasury for an aggregate price exceeding $329.8 million. This acquisition brought the company’s total holdings to an impressive 766,970 BTC. At the time of publication, valuing these holdings at prevailing market prices places their worth at approximately $54.5 billion, according to data compiled by the company itself and various tracking services like SaylorTracker.

Headquartered in Tysons Corners, Virginia, MicroStrategy has consistently demonstrated a commitment to its Bitcoin-centric corporate strategy. This unwavering dedication has seen the company continue its accumulation even during pronounced bear markets, such as the period that pushed Bitcoin’s price down to two-year lows, temporarily placing MicroStrategy’s substantial BTC treasury underwater. This long-term conviction contrasts sharply with the strategies adopted by many other corporate entities, which often de-risk or divest during market downturns.

A Historical Perspective: The Genesis of MicroStrategy’s Bitcoin Bet

MicroStrategy’s foray into Bitcoin began in August 2020, marking a pivotal shift in the company’s corporate strategy. At the time, Michael Saylor announced that the company had adopted Bitcoin as its primary treasury reserve asset, citing concerns about monetary inflation, the depreciation of fiat currencies, and the search for a superior store of value. The initial purchase of 21,454 BTC for $250 million was unprecedented for a publicly traded company and immediately garnered significant attention.

Saylor articulated a vision where Bitcoin, as a decentralized, scarce, and immutable digital asset, offered a hedge against macroeconomic uncertainties and a pathway to long-term value preservation. This foundational decision set MicroStrategy on a path to continuously integrate Bitcoin into its balance sheet, effectively transforming the enterprise software firm into a de facto Bitcoin investment vehicle for many investors. Over the subsequent months and years, MicroStrategy utilized various financing mechanisms, including convertible senior notes and equity offerings, to fund its escalating Bitcoin acquisitions. This approach allowed the company to leverage its balance sheet and access capital markets to further its Bitcoin strategy without significantly diluting its core business operations.

Navigating Volatility: Unrealized Losses and Long-Term Vision

Despite its long-term conviction, MicroStrategy has not been immune to the inherent volatility of the cryptocurrency market. The company’s average cost of acquisition for its extensive Bitcoin holdings stands at approximately $75,644 per BTC. At the time of this writing, with Bitcoin’s market price hovering below this figure, MicroStrategy is currently reporting substantial unrealized losses on its holdings. For the first quarter of 2026, the company recorded a loss of nearly $14.5 billion on its Bitcoin investments, as detailed in a filing with the U.S. Securities and Exchange Commission (SEC). This figure underscores the magnitude of the price fluctuations inherent in Bitcoin and the substantial exposure MicroStrategy has taken on.

However, Michael Saylor and MicroStrategy’s management have consistently framed these fluctuations as short-term noise within a long-term investment thesis. Saylor has frequently reiterated his belief that Bitcoin is "digital capital" and that its long-term growth trajectory is driven by fundamental capital flows rather than traditional four-year halving cycles alone. In an April statement, Saylor emphasized, "The global consensus is that BTC is digital capital. The four-year cycle is dead. Price is now driven by capital flows. Bank and digital credit will determine Bitcoin’s growth trajectory." This philosophical underpinning guides the company’s continued accumulation strategy, viewing dips as opportunities to acquire more of what they consider a pristine, inflation-resistant asset.

The Supply Squeeze Narrative: MicroStrategy vs. Miners

MicroStrategy’s aggressive accumulation strategy has given rise to a compelling narrative within the Bitcoin community: the potential for a supply squeeze. The company’s rate of acquisition has, at various points, significantly outpaced the rate at which new Bitcoin is mined and introduced into circulation. For instance, in March, Bitcoin miners collectively produced approximately 16,200 BTC. During that same period, MicroStrategy accumulated an astonishing 46,233 BTC, which is nearly three times the newly mined supply.

This disparity highlights the immense buying pressure exerted by MicroStrategy alone. When combined with other institutional demand, such as that from spot Bitcoin Exchange-Traded Funds (ETFs) and other corporate treasuries, the argument for a potential supply squeeze gains considerable traction. The Bitcoin halving events, which periodically reduce the supply of newly minted Bitcoin by half, further amplify this dynamic. With the most recent halving having occurred, the already constrained supply of new Bitcoin makes MicroStrategy’s continued large-scale purchases even more impactful on market dynamics. Analysts suggest that if such accumulation rates persist, the finite supply of Bitcoin could face significant upward price pressure as demand continues to outstrip available supply.

Financing the Bitcoin Empire: Convertible Notes and Equity Offerings

To fund its ambitious Bitcoin acquisition program, MicroStrategy has creatively leveraged its corporate structure and access to capital markets. The primary methods employed have been the issuance of convertible senior notes and the sale of its own equity. Convertible senior notes are a form of debt that can be converted into a predetermined number of shares of the company’s stock under certain conditions. This allows MicroStrategy to raise capital with potentially lower interest rates than traditional debt, while also offering investors an upside if the company’s stock (which is heavily influenced by Bitcoin’s price) performs well.

Since its initial Bitcoin purchase in 2020, MicroStrategy has conducted numerous offerings of these convertible notes, raising billions of dollars specifically earmarked for Bitcoin acquisitions. For example, in March of this year, the company announced two separate convertible senior notes offerings, aiming to raise a combined total of over $1.3 billion, with the explicit intention of using the net proceeds to purchase more Bitcoin. Additionally, MicroStrategy has also utilized at-the-market (ATM) equity offerings, selling shares of its common stock to raise capital. This strategy allows the company to capitalize on investor demand for Bitcoin exposure through its stock, using the proceeds to directly acquire the underlying asset. While these financing methods have been effective in fueling MicroStrategy’s Bitcoin treasury, they also introduce financial complexities and risks, including interest rate exposure and potential shareholder dilution.

A Contrarian Approach: MicroStrategy vs. Industry Peers

MicroStrategy’s steadfast accumulation strategy stands in stark contrast to the actions of many other companies within the cryptocurrency ecosystem, particularly during challenging market conditions. While MicroStrategy doubles down on its Bitcoin bet, some peers have shown signs of "capitulation" or have pivoted their strategies amid a demanding business environment.

A notable example is MARA Holdings (Marathon Digital Holdings), a significant Bitcoin mining company. In March, MARA Holdings sold 15,133 Bitcoin for approximately $1.1 billion. This substantial sale was not for profit-taking in the traditional sense, but rather to repurchase $1 billion of zero-coupon convertible notes at a discount. Fred Thiel, Chairman and CEO of MARA Holdings, stated that this transaction was aimed at enhancing the company’s "financial flexibility" and increasing its "strategic optionality" as MARA looks to expand "beyond pure-play Bitcoin mining into digital energy and AI/HPC infrastructure." This strategic shift by MARA highlights a divergence in corporate philosophy, with some companies opting to diversify or optimize their balance sheets, while MicroStrategy remains singularly focused on Bitcoin accumulation. This contrast further solidifies MicroStrategy’s unique position as a leading proponent of a maximalist Bitcoin treasury strategy.

The Broader Market Impact and MSTR as a Bitcoin Proxy

MicroStrategy’s unprecedented Bitcoin strategy has had profound implications beyond its own balance sheet. Its stock, MSTR, has become a popular proxy for Bitcoin exposure for institutional investors and those who prefer to invest in regulated equity markets rather than directly in cryptocurrencies. The performance of MSTR shares is often highly correlated with the price movements of Bitcoin, making it an unofficial spot Bitcoin ETF long before the official ones were approved.

This "Saylor effect" has also influenced corporate adoption discussions. MicroStrategy’s willingness to take such a significant position, and its detailed explanations for doing so, provided a roadmap and a degree of legitimacy for other companies considering adding Bitcoin to their balance sheets. While few have matched MicroStrategy’s scale, the company’s actions have undoubtedly contributed to a broader acceptance of Bitcoin as a legitimate corporate treasury asset. However, the strategy also carries inherent risks, including the extreme volatility of Bitcoin, potential regulatory changes, and the financial leverage used to acquire its holdings. Critics often point to these risks, questioning the long-term sustainability of such a concentrated bet.

Future Outlook and Saylor’s Macro Thesis

With its current reserve of 766,970 BTC, MicroStrategy firmly holds the top position as the largest Bitcoin treasury company by holdings, significantly dwarfing the next largest, Twenty One Capital, which holds 43,514 BTC, according to BitcoinTreasuries data. This dominant position underscores the scale and ambition of Saylor’s vision.

Looking ahead, Michael Saylor’s statements suggest that MicroStrategy will continue to adhere to its "Bitcoin strategy," viewing Bitcoin as a long-term strategic asset. His macro thesis posits that Bitcoin represents the future of money and digital property, a superior asset class in a world grappling with inflation and economic uncertainty. The company’s ongoing commitment, despite market downturns and unrealized losses, signals a deep-seated conviction in Bitcoin’s ultimate value proposition. As the global financial landscape continues to evolve, MicroStrategy’s audacious bet on Bitcoin will remain a closely watched experiment, with its trajectory offering insights into the broader adoption and maturation of digital assets within corporate finance. The continuous "Think bigger" mantra from Saylor indicates that MicroStrategy is prepared to seize further opportunities to expand its Bitcoin treasury, reinforcing its position as a unique and influential player in both the technology and cryptocurrency sectors.