Stablecoins are positioned to significantly benefit from the burgeoning landscape of artificial intelligence (AI)-driven payments over the long term, even as their current adoption in this specific domain remains limited and subject to scrutiny. This assessment comes from a recent report by Bernstein, a prominent global research and brokerage firm, which highlighted the transformative potential of stablecoins in enabling a future of autonomous, machine-to-machine (M2M) financial transactions. The report, shared in a Monday note, delves into the intricate interplay between the stability and programmability of stablecoins and the emerging requirements of AI agents operating independently of human intervention. While the immediate impact is minimal, the strategic infrastructure being developed points to a future where stablecoins could be indispensable for the AI economy.

The Vision of Autonomous Payments: Unlocking Machine-to-Machine Economies

At the core of Bernstein’s optimistic outlook is the unique capability of stablecoins to facilitate microtransactions and enable highly programmable, conditional payments between software agents. This paradigm shift envisions a future where AI systems can autonomously pay for data, cloud services, API calls, or even physical goods and services without requiring human oversight for each individual transaction. Such a system could drastically reduce operational costs, enhance efficiency, and unlock entirely new economic models for digital services.

The need for such an infrastructure is becoming increasingly apparent as AI models grow in complexity and autonomy. These agents, whether performing tasks like data analysis, content generation, or managing supply chains, often require frequent, small payments to access resources or compensate other agents for services rendered. Traditional payment systems, with their associated fees, settlement times, and manual intervention requirements, are largely unsuited for this high-frequency, low-value transaction environment. Stablecoins, designed for digital native transactions with lower fees and near-instant settlement on blockchain networks, are seen as a natural fit to bridge this gap, offering a robust and programmable financial layer for the AI economy. Their inherent stability, pegged to fiat currencies like the U.S. dollar, makes them suitable for predictable, automated transactions, avoiding the volatility associated with other cryptocurrencies.

Early Forays and Limited Traction in AI-Driven Payments

Despite the compelling theoretical advantages, Bernstein’s analysis also underscored the nascent stage of stablecoin adoption within the AI payments sector. Current transaction volumes, while indicative of ongoing development, are still relatively modest. For instance, the machine payments protocol developed by Stripe and Tempo, two significant players in the fintech and blockchain space, recorded approximately $5,000 in stablecoin volume during its inaugural week of operation. This initial figure, though small, represents an important proof of concept for the viability of such systems.

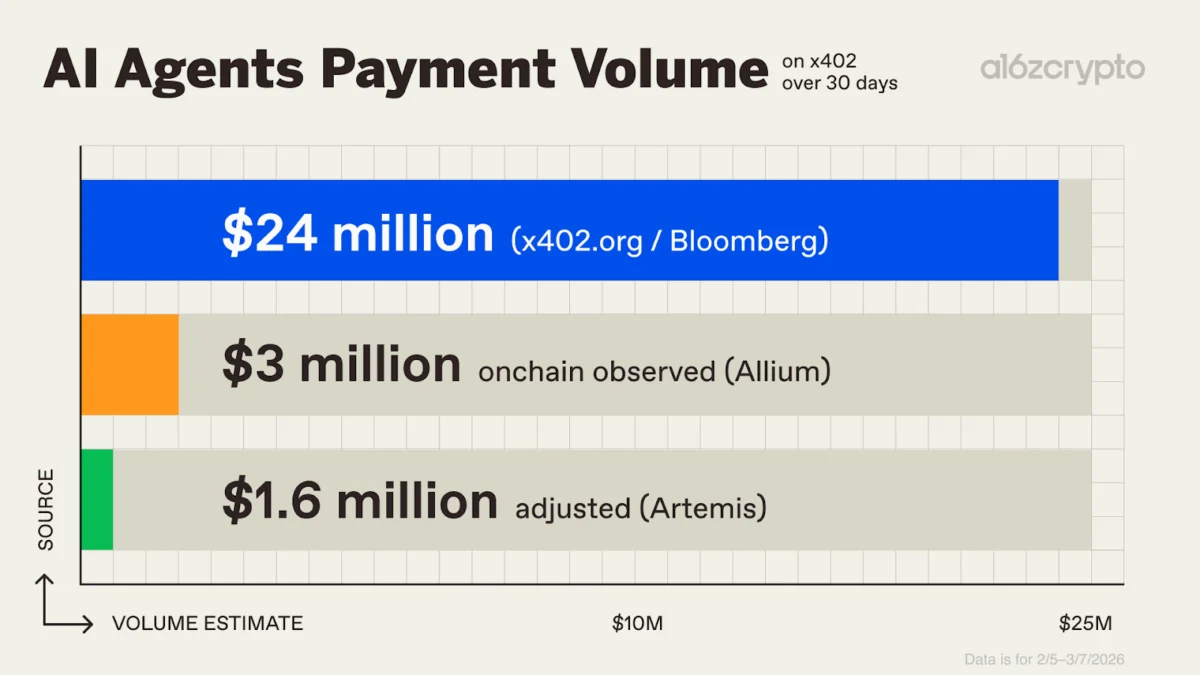

Similarly, Coinbase’s x402 protocol, a payment standard specifically designed to allow AI agents to automatically make payments over the internet, handled no more than $25 million in volume over the past 30 days, with Bernstein’s chart placing the exact figure closer to $24 million during that period. These figures, while insignificant in the broader context of global payments, represent foundational steps in building the infrastructure for autonomous financial interactions. The x402 protocol, for example, is a testament to the industry’s proactive efforts to define and standardize how AI agents will engage with monetary systems. It provides a crucial framework for machine-to-machine payments, enabling a future where digital entities can transact seamlessly and securely.

Key Industry Players Drive Innovation in AI Payments

The push towards AI-driven payments is not confined to a few niche players but is gaining momentum across the financial and tech landscape. This report follows a series of significant announcements and product launches demonstrating growing interest in autonomous payment solutions. Just days prior to Bernstein’s note, Visa’s crypto division unveiled a new tool specifically designed to enable AI agents to execute same-day payments, signaling a strategic move by a traditional payments giant into the decentralized finance (DeFi) and AI space. This initiative by Visa, a company with unparalleled reach in global payments, underscores the perceived long-term importance of integrating AI capabilities with financial transactions, potentially laying the groundwork for a massive expansion of automated commerce.

Concurrently, Tempo, a blockchain and payment protocol backed by Stripe, also launched its own blockchain and payment protocol, aiming to provide a robust infrastructure for programmable money. Tempo’s focus on creating a specialized blockchain for these transactions highlights the need for dedicated, high-throughput environments for M2M interactions. These parallel developments from established financial entities and innovative tech companies highlight a concerted effort to lay the groundwork for a future where AI agents are not just consumers of data but active participants in the economy, capable of independently managing their finances. The synergy between these new protocols and stablecoins is expected to be a critical factor in their success, leveraging the stability and efficiency of digital dollars for autonomous operations.

The Broader Stablecoin Growth Narrative: Beyond AI

Crucially, Bernstein emphasized that stablecoins do not require the immediate success of AI-driven payments to continue their impressive growth trajectory. The firm’s analysis highlighted that the demand for stablecoins is already robust and expanding rapidly due to several well-established use cases. These include cross-border business payments, which benefit from the speed and lower costs compared to traditional wire transfers; remittances, offering a more efficient and transparent way for individuals to send money internationally, particularly in emerging markets where traditional banking infrastructure may be limited; card-linked products, integrating stablecoins into everyday spending through debit cards and other financial instruments; and the rise of neobanking services that leverage stablecoins for enhanced user experience, global reach, and innovative financial products.

This existing demand forms the "core thesis" for stablecoin adoption, with AI payments representing a significant "upside case" rather than the primary driver of current growth. Bernstein’s report estimates that total stablecoin payment volume is projected to surge from $213 billion in 2024 to an impressive $375 billion in 2025. This growth is anticipated to be led primarily by consumer-to-consumer (C2C) flows, reflecting the increasing comfort and utility users find in stablecoins for peer-to-peer transactions. Additionally, business-to-consumer (B2C), business-to-business (B2B), and consumer-to-business (C2B) activities are also expected to see substantial increases, further solidifying stablecoins’ role in the broader digital economy. This diversification of use cases provides a strong foundation for stablecoin market expansion, insulating it from the slower initial uptake in specialized AI payment applications.

Coinbase and Circle: Proxies for Stablecoin Adoption

In the landscape of stablecoin adoption, cryptocurrency exchange Coinbase and stablecoin issuer Circle are identified by Bernstein as the "best proxies for stablecoin upside." This designation stems from their strategic partnership around USD Coin (USDC), one of the most widely used and regulated stablecoins in the market. Their collaborative efforts in issuing, distributing, and integrating USDC across various platforms position them at the forefront of the stablecoin economy, making them bellwethers for the broader market’s health and growth.

Bernstein further posits that USDC is particularly well-suited to capture a dominant share of machine-payment activity. This projection is based on several key attributes: USDC’s superior liquidity compared to other potential candidates, ensuring efficient and reliable transaction execution across various exchanges and protocols; its robust regulatory compliance, which instills greater trust and reduces operational risks for businesses and AI agents alike, especially given Circle’s commitment to transparency and regular audits; and its widespread integration across various blockchain networks and decentralized applications (dApps). These factors make USDC an attractive option for developers building autonomous payment systems, where reliability, regulatory clarity, and broad accessibility are paramount.

The market dominance of USDC, alongside Tether’s USDt, further illustrates the scale of stablecoin operations. In 2026, USDC recorded an adjusted transaction volume of $2.4 trillion, surpassing Tether’s USDt, which registered $1.4 trillion in transaction volume. These figures underscore the massive financial flows facilitated by these digital assets, highlighting their critical role in the global crypto economy and their potential as a foundational layer for future innovations like AI payments. The ongoing competition between these two giants, along with newer entrants, drives continuous innovation in terms of speed, cost, security, and compliance.

Addressing Wash Trading Concerns and Refining Early Metrics

While the narrative around AI-driven payments and stablecoins is largely optimistic, early reported metrics have faced scrutiny, particularly concerning the potential for wash trading. Wash trading involves an individual or entity simultaneously buying and selling the same asset to create misleading activity and inflate trading volumes artificially. Such practices can distort the true picture of adoption and organic growth, presenting an exaggerated sense of market activity.

Noah Levine, a partner at the venture capital firm a16z, brought this issue to light regarding the x402 protocol’s transaction volumes. After applying a sophisticated wash trading filter developed by Artemis Analytics, Levine revealed that the actual AI Agent payment volume on x402 amounted to approximately $1.6 million. This figure is significantly lower than the initial $24 million reported by news outlets, including Bloomberg, highlighting the importance of robust data analysis and filtering in nascent markets. The discrepancy underscores the challenges of accurately measuring organic activity in emerging digital payment systems.

Levine’s findings serve as a crucial reminder for investors and developers to exercise caution and apply critical analysis to early-stage metrics in rapidly evolving sectors like AI payments. While the adjusted volume is indeed a smaller number, Levine maintained an optimistic perspective on the underlying development. In a March 11 X post, he stated, "$1.6 million is not a big number. But the infrastructure being built around it is." This sentiment underscores a common theme in technological innovation: initial usage might be low, but the strategic value lies in the foundational technology and the ecosystem being developed around it. The focus, therefore, shifts from immediate transactional volume to the long-term potential enabled by the underlying architecture and its integration into broader digital platforms.

Strategic Integrations and the Foundation for Future Growth

Despite the modest initial transaction volumes, the strategic integrations of protocols like x402 signal a strong commitment from major tech players to this future. Levine’s post also highlighted that x402 was already integrated by prominent companies such as Stripe, Cloudflare, Vercel, and Google’s agent payments protocol. These integrations are highly significant. Stripe’s involvement brings its extensive payment infrastructure and developer network, potentially enabling a vast array of online businesses to implement AI-driven payments. Cloudflare and Vercel are crucial for internet infrastructure and application deployment, suggesting that x402 could become a default payment layer for many web services. Google’s interest through its own agent payments protocol further validates the long-term vision, indicating that one of the world’s largest tech companies recognizes the strategic importance of autonomous financial interactions.

These partnerships are not merely about processing current transactions but about embedding the capability for AI-driven payments into the very fabric of the internet and cloud services. By integrating these protocols, these companies are building the on-ramps and off-ramps necessary for AI agents to seamlessly interact with the financial system. This proactive development of infrastructure is a critical prerequisite for mass adoption, ensuring that when AI agents become more sophisticated and prevalent, the financial rails will already be in place to support their economic activities, from paying for API calls to purchasing complex datasets.

Broader Impact and Implications: Navigating the Future of Finance

The convergence of AI and stablecoins carries profound implications for the future of finance and the broader digital economy.

- Technological Advancement: The development of M2M payment protocols pushes the boundaries of blockchain technology, requiring enhanced scalability, security, and interoperability across different networks. Innovations in these areas, such as faster consensus mechanisms and cross-chain solutions, will benefit the entire crypto ecosystem.

- New Business Models: Autonomous payments could foster entirely new business models where AI agents act as independent economic actors, offering services, negotiating prices, and executing contracts without human intervention. This could lead to a more efficient and dynamic digital marketplace, potentially revolutionizing industries like logistics, data brokerage, and personalized services.

- Regulatory Challenges and Opportunities: The rise of AI-driven payments will undoubtedly present new challenges for regulators. Defining the legal and financial liabilities of autonomous agents, ensuring anti-money laundering (AML) compliance for M2M transactions, and establishing clear frameworks for stablecoin operations will be crucial. However, it also presents an opportunity for forward-thinking regulators to foster innovation while maintaining financial stability and consumer protection, potentially leading to more adaptive regulatory frameworks.

- Competitive Landscape: The race to dominate AI-driven payments will intensify competition between traditional financial institutions like Visa and new crypto-native players. This competition is likely to drive further innovation in payment processing, security, and user experience. The ability of stablecoins to offer a programmable, global, and cost-effective medium of exchange gives them a distinct advantage in this emerging field, forcing traditional players to innovate rapidly.

- Economic Efficiency: By automating microtransactions and removing human friction, AI-driven stablecoin payments have the potential to significantly enhance economic efficiency, reducing transaction costs and speeding up settlement times across various industries. This increased efficiency could unlock trillions in value by streamlining operations and enabling real-time economic interactions.

In conclusion, while the immediate transactional volumes for AI-driven stablecoin payments remain modest and require careful scrutiny for issues like wash trading, the long-term strategic significance cannot be overstated. Bernstein’s report paints a clear picture of a dual growth trajectory for stablecoins: robust and accelerating adoption in established use cases like cross-border payments and remittances, coupled with a promising, albeit nascent, role in powering the autonomous economies of the future. The foundational infrastructure being built by major players like Coinbase, Circle, Visa, Stripe, and Google, combined with the inherent advantages of stablecoins for programmable, efficient transactions, positions these digital assets as critical components in the evolving financial landscape driven by artificial intelligence. The journey has just begun, but the direction is clear: stablecoins are set to become an indispensable layer of the AI-powered economy, enabling a new era of automated commerce and financial interaction.