The escalating geopolitical tensions, marked by the commencement of hostilities involving Iran, have sent shockwaves through the global mining sector, triggering significant stock losses across the world’s largest companies. Since the conflict’s onset, the market capitalization of leading mining firms has contracted by nearly 30%, a dramatic downturn fueled by a sharp decline in commodity prices. Gold, silver, and copper have all entered technical bear markets, with silver experiencing a staggering 40% drop from its recent highs, and gold enduring its worst weekly performance in decades.

Commodities Enter Bear Market Territory Amidst Global Uncertainty

New York gold futures experienced a precipitous fall, trading down $225 per ounce from opening levels to $4,492 by late afternoon. This represented a 3.5% decline on the day and a more than 11% drop for the week, marking a significant downturn for the precious metal. Silver’s volatility was even more pronounced, with the precious metal trading at $67.81 in after-hours trade, a substantial 6.9% decrease from the start of Friday’s trading session.

Copper also succumbed to the broader market sell-off, ending the day down 4.0%. Last trading at $5.30 per pound ($11,690 per tonne), copper had shed 7.4% for the week. The combined decline for gold, silver, and copper has pushed these key commodities into technical bear market territory. Gold, specifically, has fallen by over $1,100, or more than 20%, from its record high set on January 29th. Silver has seen an even steeper decline, dropping 44% from its peak, while copper has relinquished nearly 20%, or more than $2,800 per tonne, from its all-time high also achieved at the end of January.

The precipitous fall in commodity prices is directly linked to the escalating geopolitical uncertainty. Investors, seeking safe havens, initially flocked to gold, driving its price to record highs. However, as the conflict intensified and concerns about global economic stability grew, a broader reassessment of asset valuations took hold. The potential for increased interest rates by central banks to combat inflation, spurred by rising energy costs associated with the conflict, has also dampened speculative appetite for commodities. Furthermore, the disruption to supply chains and the potential for reduced industrial demand in key consuming nations have contributed to the bearish sentiment.

Mining Giants Face Steep Valuations Cuts

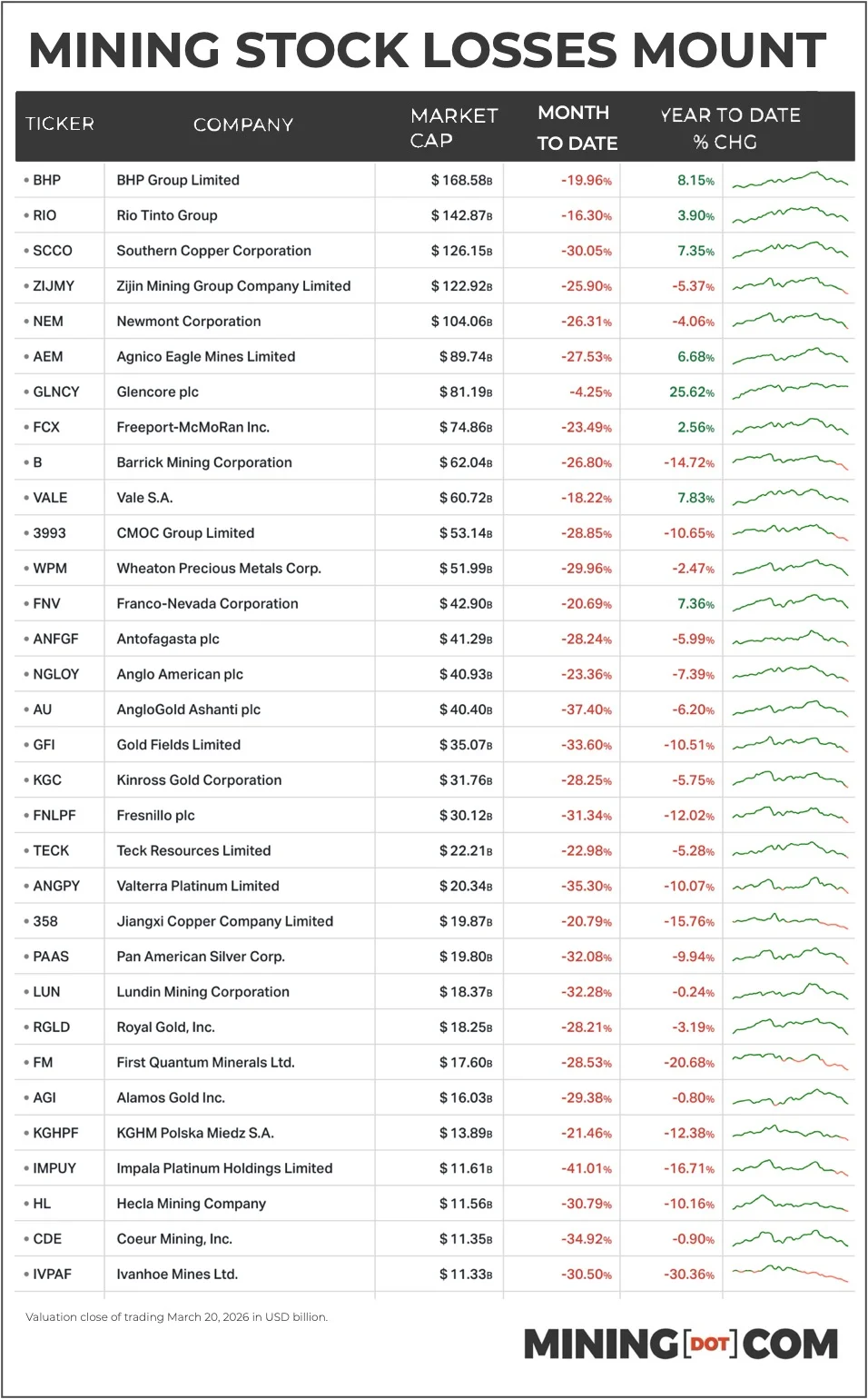

The impact on the stock prices of the world’s largest mining companies has been severe. Gold, silver, and platinum stocks have been particularly hard-hit. Newmont Corporation (NYSE: NEM), a global leader in gold mining, is now trading 26.3% below its levels prior to the onset of the Iran war at the end of February. Friday’s heavy selling saw a significant volume of 30.7 million shares traded, underscoring the market’s negative sentiment.

Barrick Gold Corporation (NYSE: ABX) has mirrored this downturn, experiencing a 26.8% decline over the same period. On Friday alone, 29.1 million shares of Barrick changed hands. Newmont’s market capitalization has shrunk from a peak of $143 billion at the end of January to $104 billion in New York. Barrick Gold has seen its market worth diminish by $27 billion since January, settling at a market capitalization of $62 billion as of Friday.

Adding to the complexities for Barrick, it was reported this week that Teck Resources holds a significant royalty on Barrick’s Fourmile gold project in Nevada. This undisclosed royalty is estimated to be worth billions of dollars and could potentially impact the valuation of Barrick’s planned North American mine spinoff. Such a development introduces an additional layer of uncertainty for investors and complicates Barrick’s strategic divestment plans.

Other major gold producers have also suffered substantial losses. Shares in Anglogold Ashanti (NYSE: AU) have plummeted by an alarming 37.4% in March alone, reducing its market value to $40 billion. Gold Fields (NYSE: GFI) has lost 33.6%, now valued at $35 billion. Kinross Gold’s stock slide has reached 28.3%, resulting in a market capitalization of $32 billion.

Royalty and streaming companies, which typically offer a more diversified exposure to mining revenues, have also felt the pinch. Wheaton Precious Metals (NYSE: WPM) has fallen just under 30% since the start of hostilities in the Middle East, now worth $52 billion. Franco-Nevada, another prominent player in this space, has experienced a more modest drop of 20.7%, with its evaluation standing at $43 billion.

Precious metal miners operating in the physical extraction space have seen even steeper declines. Over-the-counter units of silver miner Fresnillo (OTCPK: FNLPF), trading in the US, are down 31.3% in March, shrinking its market cap to $30 billion. Pan American Silver (NYSE: PAAS) has suffered a 32.1% decline, falling to under $20 billion. Valterra Platinum (OTCPK: ANGPY) has been one of the worst performers in the sector, dropping a significant 35.3% from a multi-year high reached just before the conflict began, concluding the three-week period with a market cap of $20 billion.

Diversified Miners and Copper Producers Face Significant Headwinds

While the precious metals sector has borne the brunt of the sell-off, copper producers and diversified mining companies have also experienced substantial losses, with most declining by over 20%. Only a few exceptions have managed to weather the storm with comparatively smaller losses.

BHP (NYSE: BHP), one of the world’s largest diversified miners, has seen its US-traded shares shed 20.0%. This decline comes after the company had reached a historic record valuation for any mining stock at the beginning of the war. Despite reporting record profits and benefiting from China’s sustained demand as its primary customer, BHP has not been immune to the broader fallout of the geopolitical crisis. The incoming CEO, Brandon Craig, who assumes leadership at the end of May, inherits a company balancing ambitious spending plans with investor expectations for returns, a challenging task following a period marked by bold, though not always successful, dealmaking, including its notably unsuccessful bid for Anglo American.

Southern Copper (NYSE: SCCO) has underperformed other copper majors, recording losses of 31.1% for March and a market value of $126 billion. This decline has seen the company, part of the Grupo Mexico stable, lose its position as the world’s second most valuable miner to Rio Tinto (NYSE: RIO). Rio Tinto has experienced a relatively lighter decline of 16.3%, bringing its market capitalization to $143 billion.

Rio Tinto’s stock received a boost earlier in the week following an announcement that the company has gained control of acreage in Arizona essential for the development of the Resolution mine. This project is slated to become one of the largest U.S. sources of copper. Rio Tinto has indicated plans to commence a $500 million drilling campaign to further delineate the deposit, which is co-owned with BHP. This strategic development offers a glimmer of positive news amidst the prevailing market downturn.

Freeport-McMoRan (NYSE: FCX), a major copper producer, has been one of the most actively traded mining stocks, with over 25 million shares exchanging hands. Following a 23.5% retreat in March, Freeport is now valued at $74 billion, a notable decrease from its brief ascent to the $100 billion mark in February, a milestone achieved by only a handful of mining stocks historically.

Recent reports from a Chilean business paper indicate that Freeport-McMoRan has initiated the environmental permitting process for a $7.5 billion expansion of its majority-owned El Abra copper mine in Chile. This expansion is projected to increase annual copper output by over 300,000 tonnes, a significant jump from the 91,000 tonnes produced last year. Furthermore, last month, Indonesia’s investment minister and Freeport’s local unit signed a memorandum of understanding to extend the company’s mining permit for the iconic Grasberg mine beyond 2041, signaling long-term operational stability in a key producing region.

Glencore (OTCPK: GLNCY), a diversified mining and commodity trading giant, has managed to navigate the current market turbulence with relative resilience. The company has experienced a modest loss of only 4.3% since the commencement of operations involving Iran. This stability is largely attributed to its extensive oil trading business, which is expected to benefit from rising crude and gas prices. Glencore trades approximately 4 million barrels of oil equivalent per day. Currently valued at $81 billion, Glencore stands as the best performer among the mining heavyweights year-to-date, with a commendable 25.6% advance.

Speculation among large investors in Glencore last week suggested that a recent surge in coal prices could potentially reignite discussions with Rio Tinto regarding a merger. The prospect of creating the world’s largest mining company was previously explored after meetings with leaders from both companies in Australia.

Vale (NYSE: VALE), a major iron ore and nickel producer, has seen its stock decline by 18.2%, resulting in a market capitalization of $61 billion. This performance positions it as one of the better-performing large-cap miners. Shaun Usmar, the CEO of Vale’s base metals spin-off, indicated in early March that the nickel and copper business is poised for a potential initial public offering by midyear, a timeline expedited from previous projections. Usmar noted that efforts to reduce costs, lower capital intensity, and accelerate the project pipeline are progressing at a faster pace than initially anticipated.

Anglo American (OTCPK: NGLOY) has experienced losses of 23.4% since the beginning of the month, mirroring the decline of its potential merger partner, Teck Resources (NYSE: TECK). This has resulted in Teck Resources achieving a valuation of $22 billion, compared to Anglo American’s $41 billion. Last month, Anglo American announced it is considering a third write-down of its De Beers diamond business in as many years, citing persistent weak diamond prices and the miner’s ongoing asset sales in anticipation of the proposed merger. The merger is currently under review by the EU’s antitrust body.

Smaller but prominent players in the mining sector have also faced significant selling pressure. Ivanhoe Mines (TSX: IVN), a favored stock among many investors, is now trading 30.5% lower for March, with a market capitalization of $11 billion. Copper specialist First Quantum Minerals (TSX: FQM) has seen a decline of 30.5% to $18 billion over the same period. Pink sheets of Antofagasta (OTCPK: ANFGF) and KGHM (OTCPK: KGHPF) dropped 28.2% and 21.5%, respectively, reaching market values of $41 billion and $14 billion.

Chinese heavyweight Zijin Mining (OTCPK: ZIJMY) has maintained its position as the world’s fourth most valuable mining firm, despite its US over-the-counter units plunging by 30.2% since the conflict’s inception. The company currently holds a market value of $123 billion.

Broader Implications and Future Outlook

The current market turmoil highlights the inherent volatility of the mining sector, which is highly sensitive to geopolitical events, commodity price fluctuations, and global economic sentiment. The sharp decline in gold, silver, and copper prices suggests a broader risk-off sentiment among investors, who are prioritizing capital preservation over speculative investments.

The impact of these stock losses extends beyond individual company valuations. It raises concerns about the financial health of the mining industry, potentially affecting future investment in exploration and development, as well as employment levels. Companies may be forced to scale back expansion plans, reduce capital expenditures, and potentially implement cost-saving measures, including layoffs.

The performance of commodity prices is intrinsically linked to global supply and demand dynamics, as well as the broader macroeconomic environment. While the current conflict has created immediate price shocks and increased uncertainty, the long-term trajectory of these commodities will depend on a multitude of factors, including the duration and resolution of the geopolitical crisis, global economic growth prospects, and the pace of the green energy transition, which is expected to drive demand for metals like copper.

The resilience of companies like Glencore, with their diversified business models and strong trading operations, offers a potential blueprint for navigating such challenging periods. For other miners, the focus may shift towards operational efficiency, cost management, and strategic asset allocation to weather the current storm and position themselves for a future recovery. The coming months will be critical in determining the sustained impact of these events on the global mining landscape and the valuations of its key players.