Regulatory uncertainty surrounding stablecoins is increasingly placing traditional banks at a significant disadvantage compared to their more agile crypto counterparts, according to Colin Butler, executive vice president of capital markets at Mega Matrix. Financial institutions have poured substantial investments into developing robust digital asset infrastructure, yet they remain largely unable to fully deploy these capabilities as lawmakers continue to deliberate on the fundamental classification of stablecoins. This legislative paralysis creates an operational quagmire for banks, whose rigorous compliance frameworks demand explicit regulatory guidance before substantial new ventures can be greenlit.

Butler articulated the dilemma facing traditional banks, stating that "Their general counsels are telling their boards that you cannot justify the capital expenditure until you know whether stablecoins will be treated as deposits, securities, or a distinct payment instrument." This fundamental lack of clarity prevents banks from moving beyond pilot programs and into full-scale commercial deployment, effectively sidelining them in a rapidly evolving digital asset landscape. The conundrum is not merely theoretical; it stems from the core operational differences between traditional finance and the decentralized crypto ecosystem.

The Regulatory Labyrinth and Banking’s Digital Dilemma

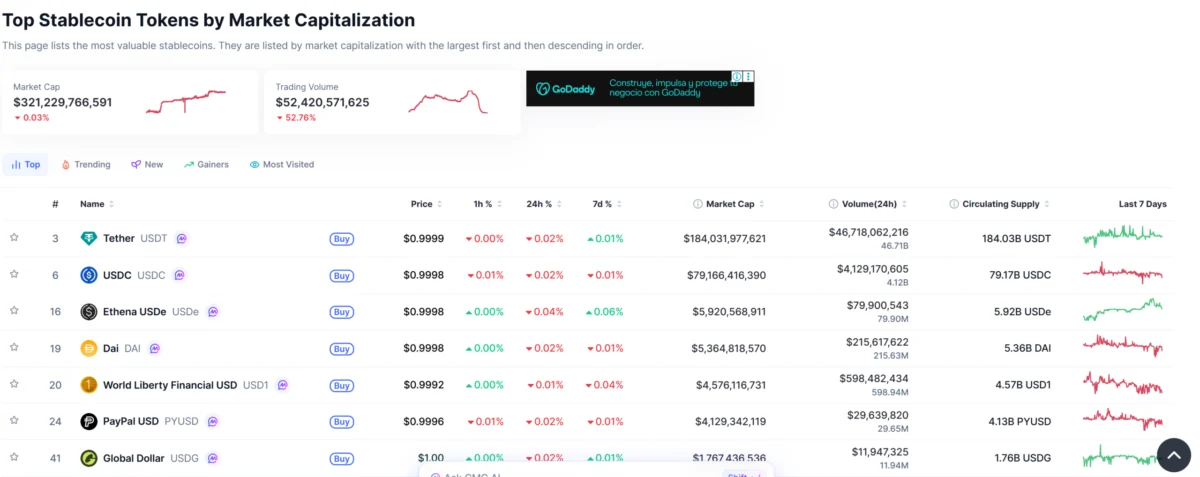

Stablecoins, digital assets designed to maintain a stable value relative to a reference asset like the U.S. dollar, have seen explosive growth in recent years. Their market capitalization soared from under $10 billion in early 2020 to over $150 billion by mid-2024, driven by their utility in facilitating faster, cheaper, and more transparent transactions within the crypto economy and increasingly as a bridge to traditional finance. This growth has caught the attention of regulators worldwide, who grapple with how to integrate these novel instruments into existing financial frameworks without compromising stability, consumer protection, or anti-money laundering (AML) efforts.

For traditional banks, engaging with stablecoins presents a complex challenge. Unlike crypto firms that often operate within loosely defined or even entirely unregulated spaces, banks are subject to stringent capital requirements, consumer protection laws, and AML/Know Your Customer (KYC) mandates that have been meticulously developed over decades. These regulations, while vital for financial stability, also create a bureaucratic hurdle when new technologies emerge without clear legal definitions. The ongoing debate in the United States, for instance, centers on whether stablecoins should be regulated as bank deposits (implying FDIC insurance and traditional banking oversight), as securities (bringing them under SEC purview), or as a new class of payment instruments (potentially requiring bespoke legislation). Each classification carries vastly different implications for capital allocation, operational procedures, and risk management.

Traditional Finance’s Digital Foothold: Investments on Hold

Despite the regulatory fog, major banks have not shied away from investing in the foundational technologies required to support digital assets and stablecoins. Their proactive approach underscores a recognition of the transformative potential of blockchain technology and tokenized assets. For example, JPMorgan, a titan in global finance, has been a trailblazer with its Onyx blockchain payments network. Launched in 2020, Onyx facilitates wholesale payments and tokenized assets, demonstrating the bank’s commitment to leveraging blockchain for institutional use cases. This initiative includes JPM Coin, a stablecoin-like digital currency designed for institutional clients to move money instantly.

Similarly, BNY Mellon, one of the world’s largest custodian banks, has launched digital asset custody services, allowing institutional clients to hold and manage cryptocurrencies and potentially stablecoins alongside their traditional assets. This move positions BNY Mellon at the intersection of traditional and digital finance, offering a crucial bridge for institutions looking to enter the space. Citigroup has also been actively exploring the potential of tokenized deposits, conducting pilot programs to test the issuance and transfer of digital representations of traditional bank deposits on a blockchain. These initiatives, while significant, are largely confined to experimental or limited-scale deployments, unable to reach their full commercial potential.

Butler reiterated this point, emphasizing that "The infrastructure spend is real, but regulatory ambiguity caps how far those investments can scale because risk and compliance functions will not greenlight full deployment without knowing how the product will be classified." The sheer volume of capital and human resources dedicated by these institutions to building out this digital infrastructure speaks volumes about their long-term vision. However, without a clear regulatory framework, these investments remain underutilized, creating a significant opportunity cost.

The Competitive Imbalance: A Tale of Two Industries

The stark contrast in operational flexibility between traditional banks and crypto firms is a central theme in this unfolding narrative. Crypto firms, many of which were born out of a desire to circumvent traditional financial intermediaries, have historically operated in regulatory "gray zones" or in jurisdictions with more permissive regulations. This environment has allowed them to innovate rapidly, launch new products, and scale quickly, often before regulators can fully comprehend or respond to their innovations. While this approach carries inherent risks, including heightened potential for fraud or systemic instability, it also grants them an agility that regulated banks simply cannot match.

"Banks, by contrast, cannot operate comfortably in that gray area," Butler highlighted. Their very existence is predicated on trust, stability, and adherence to an intricate web of rules designed to protect depositors and maintain systemic integrity. A bank’s brand reputation and regulatory license are its most valuable assets, and operating without explicit legal clarity on a new product like stablecoins could jeopardize both. This fundamental difference in operational philosophy and regulatory burden means that crypto firms can continue to push boundaries, while banks, despite their technological readiness, remain tethered by caution and compliance mandates.

The Looming Threat: Yield Gap and Deposit Migration

Beyond the immediate operational constraints, a more insidious threat looms for traditional banks: the growing disparity in yield offerings between stablecoin platforms and conventional bank accounts. This "yield gap" could trigger a significant migration of deposits, particularly from discerning investors and corporate treasuries seeking higher returns.

Stablecoin platforms, through various mechanisms such as lending programs, staking, or liquidity provision, often offer annual percentage yields (APYs) ranging from 4% to 5% on stablecoin balances. In stark contrast, the average U.S. savings account currently yields less than 0.5%, with many large banks offering rates closer to 0.01%. This ten-fold or even hundred-fold difference in potential returns creates a powerful incentive for capital to flow out of traditional banking coffers and into the digital asset ecosystem.

History offers a cautionary tale. Butler drew parallels to the shift into money market funds in the 1970s. During that era of high inflation and regulated interest rates, banks were legally restricted from offering competitive yields on traditional deposits. Money market funds, being outside these regulations, could offer significantly higher returns, leading to a massive outflow of deposits from banks into these new investment vehicles. This phenomenon, known as "disintermediation," forced banks and regulators to adapt, eventually leading to the deregulation of deposit interest rates.

Today, the potential for such a shift is even more pronounced and could occur at an unprecedented speed. The friction involved in transferring funds from a traditional bank account to a stablecoin platform has been dramatically reduced. What once took days or weeks in the 1970s can now be accomplished in minutes, thanks to instant payment rails and seamless digital onboarding processes. This ease of transfer, combined with a yield gap that is often larger than what was seen historically, creates a potent cocktail for rapid deposit migration.

Fabian Dori, chief investment officer at Sygnum, acknowledged the competitive gap as "meaningful but not yet critical." He suggested that a large-scale, immediate deposit flight is unlikely, as institutional clients, in particular, continue to prioritize factors like trust, established regulation, and operational resilience when making treasury decisions. For many, the perceived risks associated with the nascent crypto market still outweigh the allure of higher yields.

However, Dori cautioned that "the asymmetry can accelerate migration at the margin, especially among corporates, fintech users, and globally active clients already comfortable moving liquidity across platforms." These sophisticated entities are often less tethered to traditional banking relationships and are more adept at optimizing their capital for maximum returns. He added a critical insight: "Once stablecoins are treated as productive digital cash rather than crypto trading tools, the competitive pressure on bank deposits becomes much more visible." This subtle shift in perception, from speculative asset to utilitarian financial instrument, could mark a turning point for broader adoption and increased pressure on traditional banking models.

The Offshore Drift: Unintended Consequences of Yield Restrictions

Another significant concern raised by Butler pertains to the potential for regulatory overreach in restricting stablecoin yield. Attempts to ban or heavily limit yield offerings could inadvertently push legitimate financial activity into less regulated, offshore environments, ultimately undermining the very goals of consumer protection and financial stability.

Under current U.S. law, direct yield payments from stablecoin issuers to holders are generally prohibited, reflecting a cautious approach to preventing stablecoins from mimicking interest-bearing deposits without full banking oversight. However, crypto exchanges and decentralized finance (DeFi) protocols have found alternative ways to offer returns, primarily through lending programs, staking mechanisms, or promotional rewards. These indirect methods allow users to earn yield by contributing their stablecoins to various liquidity pools or lending protocols.

If lawmakers were to impose broader restrictions that effectively eliminate all avenues for earning yield on stablecoins within regulated domestic frameworks, capital would not simply cease seeking returns. As Butler succinctly put it, "Capital doesn’t stop seeking returns." Instead, it would likely migrate to alternative structures and jurisdictions. One emerging example is synthetic dollar tokens, such as Ethena’s USDe. These products generate yield not through traditional reserves or lending but through sophisticated derivatives markets, often involving delta-hedging strategies on underlying cryptocurrencies. These mechanisms can continue to offer attractive returns even if regulated fiat-backed stablecoins are stripped of their yield-generating capabilities.

Such a scenario would present a significant challenge for regulators. If a substantial portion of stablecoin activity, particularly that driven by yield-seeking, shifts to opaque offshore structures or complex synthetic instruments, regulators could face the opposite outcome of their intentions. Instead of creating a safer, more transparent environment, they might inadvertently foster a shadow banking system for digital assets, characterized by fewer consumer protections, increased systemic risk, and greater difficulty in monitoring illicit financial flows. This highlights the delicate balance regulators must strike between fostering innovation and mitigating risk without stifling legitimate economic activity or driving it underground.

Broader Implications for the Financial System

The ongoing regulatory uncertainty around stablecoins carries profound implications for the future of the global financial system. The debate is not merely about classifying a new digital asset; it is about defining the future role of banks, the nature of money, and the architecture of global payments.

If traditional banks remain hobbled by a lack of clear guidance, they risk falling further behind crypto-native firms that are unburdened by legacy systems and stringent compliance requirements. This could accelerate the disintermediation of traditional finance, with a growing share of financial services, particularly payments and lending, shifting to decentralized or quasi-centralized digital platforms. Such a shift could challenge the existing financial stability framework, as traditional regulatory tools may not be effective in supervising a fragmented and rapidly evolving digital ecosystem.

Moreover, the competition for deposits and liquidity could intensify dramatically. Banks, already facing challenges from non-bank financial institutions, could see their traditional funding sources erode, impacting their ability to lend and support economic growth. The development of central bank digital currencies (CBDCs) is also part of this broader conversation, with some arguing that CBDCs could offer a regulated, stable digital alternative to private stablecoins, while others express concerns about their potential impact on commercial banks and financial privacy.

Ultimately, the imperative for regulatory clarity is paramount. A well-defined, proportionate, and adaptable regulatory framework for stablecoins is essential not only to level the playing field for traditional banks but also to harness the potential benefits of these digital assets while safeguarding consumers and maintaining financial stability. Without it, the current chasm between traditional finance and crypto innovation will only widen, with potentially far-reaching consequences for the global economy. The longer lawmakers delay, the greater the risk that the traditional financial system will find itself increasingly marginalized in the digital age.