The global passenger electric vehicle (EV) market, encompassing both plug-in and conventional hybrid models, surpassed 30 million units sold last year, marking a substantial year-over-year growth of 18%. A more critical metric for understanding demand in the battery materials sector, the combined battery capacity deployed, expanded by an even more impressive 22%. This surge in battery deployment signals a pivotal moment for the EV industry and its critical supply chains.

According to data compiled by Adamas Intelligence, a Toronto-based advisory firm specializing in the EV supply chain, 2025 marked the first calendar year where the total deployed battery capacity exceeded one terawatt-hour (TWh). To contextualize this achievement, in 2021, the global market’s deployed battery capacity stood at 286 gigawatt-hours (GWh). This means the EV battery market, measured by capacity, has nearly quadrupled in just four years, and is an astounding ten times larger than it was in 2019, demonstrating remarkable resilience and growth even amidst the global pandemic.

A Turnaround in Battery Metals Demand

While unit sales provide a headline figure, the EV Metal Index, which tracks both the demand for and prices of key metals within the EV battery supply chain, offers a more nuanced perspective. This index has illuminated the significant slump experienced by raw material suppliers in recent years. However, even by this measure, the outlook has considerably brightened. The aggregate cost of lithium, graphite, nickel, cobalt, and manganese contained within the batteries of EVs sold throughout 2025 climbed to $15.6 billion, an 11% increase from the previous year.

While $15.6 billion might appear modest in the grand scheme of global commodity markets, it’s crucial to note that this figure represents the value of materials contained within the batteries. It does not account for the substantial losses incurred during processing, chemical conversion, and battery production scrap, where yield losses can often reach double-digit percentages, and even higher rates during initial production ramp-ups. Consequently, the actual required tonnage and the associated revenues at the supply chain’s entry points are significantly higher.

This $15.6 billion figure, though a significant rebound, still represents less than half of the extraordinary peak reached in 2022. However, projections indicate that 2026 is poised to continue this trajectory of strong growth. This positive outlook is underpinned by the sustained rise in lithium and nickel prices, which are gradually making their way through the supply chain, while cobalt prices are also showing upward momentum.

The Evolving Chemistry of EV Batteries

The landscape of battery chemistries is in constant flux, influencing the demand for specific raw materials. Lithium and graphite have remained relatively constant staples in EV battery technology. However, the demand for nickel and cobalt has been significantly impacted by two parallel trends. Automakers are actively "thrifting" cobalt in NCM (nickel-cobalt-manganese) and NCA (nickel-cobalt-aluminum) batteries, reducing its proportion. Simultaneously, there has been an accelerating adoption of LFP (lithium-iron-phosphate) cathode chemistries, which entirely eschew cobalt and often nickel.

In 2025, LFP battery packs accounted for nearly half of the total deployed battery capacity. This dominance is particularly pronounced in China, where LFP batteries now command a substantial and growing market share of 70%. While LFP’s penetration in North American and European markets has been slower, partly due to the time required to establish localized production, its cost advantages are beginning to gain traction.

The negative impacts of LFP’s intrusion into Western markets are being partially offset by a concurrent trend towards higher nickel content NCM batteries. These batteries, often featuring 60% or more nickel, and increasingly 80% and above, remain the preferred chemistry outside of China, especially for performance-oriented vehicles. This dual evolution in battery chemistry highlights the complex interplay between cost, performance, and material sourcing strategies.

Automaker Spending Patterns: A Tale of Two Strategies

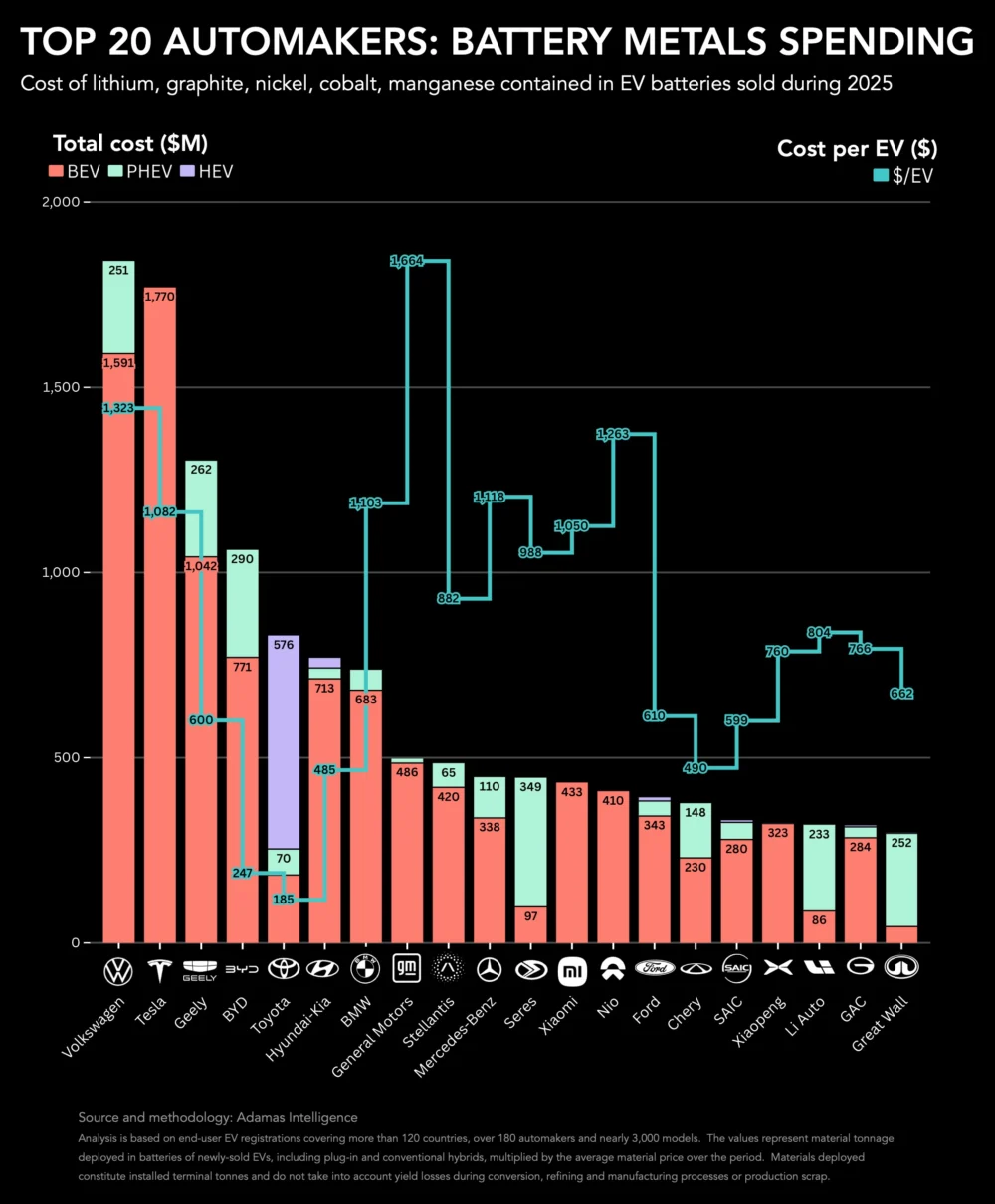

A closer examination of individual automakers reveals significant disparities in battery metals usage and associated costs. Despite selling approximately 500,000 more full electric vehicles (BEVs) than Tesla last year, and an additional 2.2 million plug-in hybrids, BYD’s total battery materials bill was $710 million less than its Texas-based competitor. BYD’s in-house manufactured batteries cost the Chinese company approximately $1.1 billion in 2025, a figure that remained stable compared to 2024, despite selling 230,000 more BEVs and PHEVs year-over-year.

BYD’s strategy of exclusively utilizing lithium-iron-phosphate (LFP) batteries, coupled with a product lineup concentrated at the lower end of the market and a sales mix now heavily weighted towards plug-in hybrids, has resulted in remarkably low sales-weighted average material costs per EV. BYD’s cost per EV stood at a mere $247, a stark contrast to Tesla’s $1,082 per model sold. Even when considering only fully electric vehicles, BYD’s raw material expenditure averaged a competitive $366 per BEV. While Tesla does incorporate LFP-powered Model 3 and Y vehicles into its sales mix, particularly those manufactured in China, the slower build-out of LFP cell factories outside of China means these nickel, cobalt, and manganese-free power packs are still largely absent from the lineups of Western automakers.

The Volkswagen Group, which encompasses brands like Audi, Porsche, and Skoda, presents a different picture. For the Volkswagen stable, the average battery metals cost per BEV reached $1,624. This figure positions Volkswagen as the world’s largest spender on battery metals for the first time. The group’s EV sales are split approximately 70% BEV and 30% PHEV, which contributes to its higher expenditure. However, the bulk of Volkswagen’s budget is allocated to battery nickel and cobalt. In response to the cost advantages of LFP, Volkswagen’s PowerCo subsidiary has commissioned an LFP battery plant in Germany and is constructing another in Spain, with production anticipated to commence next year. This move signals a strategic shift to capture the cost efficiencies offered by LFP technology.

General Motors and Toyota: Divergent Paths

Moving up the expenditure scale, General Motors faces an average battery metals bill of $1,664 per EV, representing a substantial 17.6% increase year-on-year. This rise is attributed to increased utilization of nickel and cobalt, alongside a 20% surge in EV shipments driven by popular models like the Equinox SUV and the Silverado pickup. Approximately 85% of GM’s battery capacity, measured on a GWh basis, is sourced from its joint venture with LG Energy Solution, known as Ultium. However, GM is undergoing a strategic overhaul, spurred by the recruitment of a former Tesla battery executive in 2024. The company is moving away from its heavy, one-size-fits-all battery packs and is actively exploring different battery chemistries. While GM has historically favored NCMA (nickel-cobalt-manganese-aluminum) batteries, the compelling cost savings associated with LFP have prompted the company to retrofit its Tennessee NCMA plant to produce LFP batteries. This strategic pivot underscores the growing influence of LFP technology on established automakers.

On the other end of the spectrum, Toyota has maintained a remarkably low average battery metals expenditure of just $185 per EV sold in 2025, totaling $830 million for the year. This represents a modest 7.2% increase year-on-year. Toyota’s strategy has predominantly focused on conventional hybrids (HEVs), where battery capacity typically does not exceed 2 kWh. Last year, nine out of every ten electrified vehicles sold by Toyota, including its Lexus luxury brand, were HEVs. These vehicles primarily utilize nickel-metal-hydride (Ni-MH) batteries. This continued reliance on HEVs, exemplified by the enduring popularity of the Prius and its successors, signifies that traditional hybrid technology remains a meaningful source of demand for battery nickel, alongside a significant requirement for rare earth elements.

Implications for the Battery Supply Chain

The diverging strategies of major automakers have profound implications for the global battery supply chain. The surging demand for battery capacity, now exceeding 1 TWh annually, necessitates massive investments in mining, refining, and battery manufacturing. The increasing adoption of LFP batteries, while reducing reliance on cobalt and often nickel, places a greater emphasis on lithium and graphite production. Conversely, the continued development of high-nickel NCM batteries will sustain demand for nickel, a critical component in many regions’ electrification goals.

The significant cost differential between automakers like BYD, heavily invested in LFP, and those like Volkswagen and General Motors, transitioning towards it, highlights the competitive advantages that can be gained through strategic battery chemistry choices. As LFP production capacity expands globally, it is expected to exert downward pressure on the cost of battery packs, potentially accelerating EV adoption rates.

The robust growth in battery capacity deployed underscores the critical importance of securing stable and sustainable sources of battery metals. Geopolitical considerations, environmental regulations, and the need for ethical sourcing are becoming increasingly prominent factors in supply chain management. The industry’s trajectory suggests a continued, albeit evolving, demand for a range of battery metals, necessitating ongoing innovation in extraction, processing, and recycling technologies. The coming years will likely see further shifts in material demand as automakers refine their battery strategies in pursuit of cost efficiency, performance, and sustainability.