The delicate geopolitical landscape of the Middle East is casting a long shadow over global commodity markets, with escalating tensions directly contributing to a sharp rise in oil prices. This surge in crude oil prices, as highlighted in a recent comprehensive report by BMO Capital Markets, poses a significant threat to the mining industry, poised to drive up operational expenses and put considerable pressure on already tight sector margins. The report, which meticulously analyzes historical cost trends utilizing data from Wood Mackenzie, reveals a pronounced correlation between rising crude prices and mining expenditures, though the degree of impact varies considerably across different commodities.

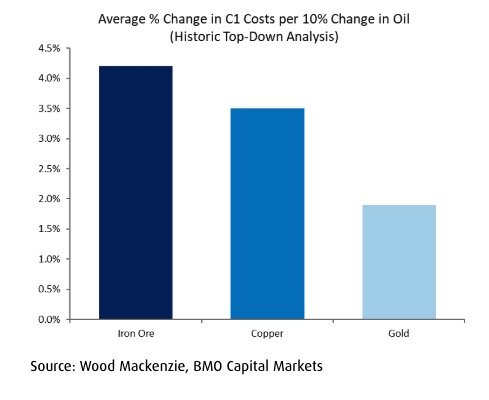

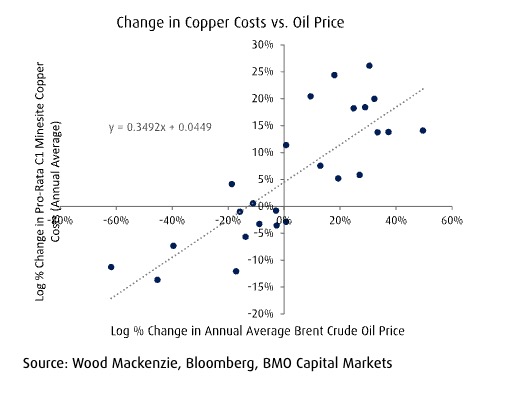

Iron ore operations emerge as the most susceptible to fluctuations in oil prices. The analysis indicates that for every 10% increase in crude oil prices, iron ore mining costs are projected to escalate by approximately 4.2%. Copper extraction follows, with costs expected to rise by roughly 3.5% for a similar 10% jump in oil prices. Gold mining operations, while less exposed than iron ore and copper, are still predicted to see a cost increase of about 2% for every 10% rise in crude. Projections within the report paint a stark picture: if crude oil prices were to stabilize around $100 per barrel – a figure nearly 47% higher than the average anticipated for 2025 – mining costs could experience substantial increases. Specifically, iron ore costs could climb by approximately 20%, copper by 16%, and gold by 9%. This scenario underscores the inherent vulnerability of the mining sector to energy market volatility, a vulnerability that is amplified by current geopolitical uncertainties.

A Chronology of Rising Tensions and Market Reactions

The current inflationary pressures on oil prices are not a sudden phenomenon but rather a culmination of a series of geopolitical events and policy decisions that have destabilized global energy markets. The conflict in Eastern Europe, beginning with the full-scale invasion of Ukraine by Russia in February 2022, served as a significant initial shockwave. This led to widespread sanctions against Russia, a major global oil producer, disrupting established supply chains and prompting a scramble for alternative sources. The subsequent decisions by OPEC+ nations, often seen as aligning with broader geopolitical interests, to curb production have further tightened supply, contributing to sustained price increases.

More recently, renewed tensions in the Middle East, particularly concerning maritime security in vital shipping lanes such as the Strait of Hormuz, have added another layer of anxiety to the market. The presence of naval assets from various nations, including the US Marine Corps observed on board the USS John P. Murtha (LPD 26) in the Strait of Hormuz in 2019 – a testament to the region’s historical significance as a strategic chokepoint – underscores the persistent undercurrent of potential conflict. These incidents, whether involving naval patrols, drone attacks, or diplomatic standoffs, invariably raise concerns about the uninterrupted flow of oil from a region that supplies a substantial portion of the world’s energy needs.

On Friday, Brent crude prices indeed held firm above the $100 per barrel mark, demonstrating the market’s sensitivity to these ongoing concerns. This resilience in pricing occurred even as the United States implemented a temporary easing of sanctions on Russian oil. A specific license, published on the U.S. Treasury website, permits Russian crude and petroleum products loaded onto vessels before March 12 to proceed to their destinations, with this allowance extending until April 11. While intended to alleviate some immediate market pressure, this measure highlights the complex interplay of sanctions, energy supply, and geopolitical considerations. The very existence of such a license, and the limited duration of its applicability, signals that the underlying supply constraints and geopolitical risks remain largely unaddressed, thus maintaining upward pressure on oil prices.

Beyond Direct Fuel Costs: The Ripple Effect on Mining Operations

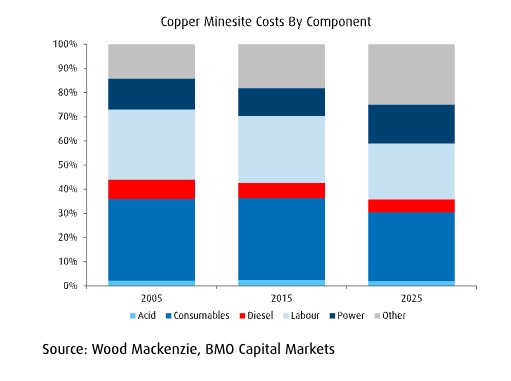

The BMO Capital Markets report critically points out that traditional "bottom-up" cost analyses often fail to capture the full impact of rising energy prices. These analyses tend to focus narrowly on direct fuel consumption, such as diesel, which has seen its direct share in operating costs decrease. For instance, diesel now accounts for only about 5% of copper mine operating costs, a notable decline from roughly 8% two decades ago. However, the analysts emphasize that higher energy prices propagate through the entire economic system, creating a cascading effect that amplifies overall cost pressures.

This ripple effect manifests in several key areas:

- Electricity: Increased oil prices invariably lead to higher electricity generation costs, especially in regions reliant on fossil fuel power plants. Mines consume vast amounts of electricity for operations such as ventilation, pumping, crushing, and grinding.

- Consumables: The production and transportation of virtually all mining consumables, from explosives and reagents to lubricants and spare parts, are energy-intensive. Higher fuel prices translate directly into increased costs for these essential supplies.

- Labour: While not directly tied to oil prices, sustained inflation driven by energy costs can lead to demands for higher wages to compensate for the increased cost of living, thus impacting labor expenses.

- Equipment: The manufacturing and maintenance of heavy mining machinery are reliant on energy and transportation. Higher energy costs can increase the price of new equipment and the cost of repairs and servicing.

- Transportation and Logistics: The movement of raw materials, finished products, and personnel is heavily dependent on fuel. Elevated oil prices directly impact shipping, trucking, and air freight costs, affecting both inbound supply chains and outbound product distribution.

This interconnectedness means that even if a mine has invested in fuel efficiency or reduced its direct diesel consumption, it remains exposed to the broader inflationary pressures driven by energy costs across its entire value chain.

Commodity-Specific Sensitivity: A Deeper Dive

The BMO report provides a detailed breakdown of how different commodities are affected:

- Iron Ore: The high sensitivity of iron ore mining to oil prices is largely attributed to the energy-intensive nature of bulk commodity extraction and transportation. Large-scale open-pit mining operations rely heavily on heavy-duty vehicles for hauling ore, and the export of iron ore, often over long distances, incurs significant shipping costs.

- Copper: Copper mining, particularly in its later stages of processing like solvent extraction and electrowinning, also exhibits considerable energy dependence. While direct diesel use may have decreased, the overall energy footprint for electricity, chemical inputs, and smelting remains substantial.

- Gold: Gold mining, while still impacted, shows a comparatively lower sensitivity. This can be due to a variety of factors, including the higher value-to-weight ratio of gold, which makes transportation costs a smaller proportion of overall production costs, and potentially more diversified energy sources or greater adoption of energy-efficient technologies in some operations.

The report’s figures, derived from Wood Mackenzie data, offer concrete metrics for understanding this differential impact:

| Commodity | Cost Sensitivity to Oil Price (per 10% rise) |

|---|---|

| Iron Ore | ~4.2% |

| Copper | ~3.5% |

| Gold | ~1.9% |

These percentages illustrate that a sustained period of oil prices at or above $100 per barrel could fundamentally alter the economic viability of certain mining projects, particularly those with higher operating costs or those producing lower-margin commodities.

Regional Variations and Mitigating Factors

The impact of rising oil prices is not uniform across the globe. The BMO report highlights significant regional differences in cost sensitivity:

- Africa and the Americas: Mines in these regions have historically demonstrated lower sensitivity to global oil price fluctuations. This is often attributed to greater access to cheaper, locally sourced fuel supplies and more affordable domestic power generation options.

- Europe and Asia: Operations in these continents tend to be more sensitive, potentially reflecting a greater reliance on imported fossil fuels and a more interconnected energy market.

However, the mining industry is not standing still. Over the past two decades, companies have actively pursued strategies to reduce their vulnerability to energy price shocks. These include:

- Fuel Efficiency Improvements: Investing in newer, more fuel-efficient fleets of vehicles and equipment.

- Electrification: Transitioning to electric-powered mining equipment and vehicles where feasible, reducing direct reliance on diesel.

- Captive Power Generation: Developing or investing in on-site power generation facilities, such as renewable energy projects (solar, wind) or even dedicated natural gas plants, to secure more stable and predictable energy costs.

- Energy Hedging: Engaging in financial instruments to lock in energy prices for a specified period, providing a buffer against short-term market volatility.

Despite these efforts, the sheer magnitude of potential price increases and the interconnectedness of global supply chains mean that no mining operation is entirely immune to the effects of sustained high oil prices.

Supply Chain Risks Beyond Direct Energy Consumption

The geopolitical instability in the Middle East introduces additional supply chain risks that can indirectly impact mining costs, even beyond direct energy expenditures. For instance:

- Sulphur Prices: Tensions in the region can disrupt the supply of sulphur, a key component in the production of sulphuric acid. Copper solvent extraction and electrowinning operations are heavily reliant on sulphuric acid. An increase in sulphur prices, therefore, directly translates to higher operating costs for copper producers.

- Ammonia Exports: A significant portion of global ammonia exports, crucial for the production of ammonium nitrate used in mining explosives, passes through the Strait of Hormuz. Any disruption to this shipping lane could lead to shortages and price hikes for essential blasting agents, directly impacting mining efficiency and cost.

The International Energy Agency (IEA) has characterized the current geopolitical climate as creating "the largest supply disruption" in history. This assertion, coupled with the coordinated release of 400 million barrels of oil from strategic reserves by numerous countries in an effort to stabilize markets, underscores the gravity of the situation and the potential for further market dislocations.

Implications for the Future of Mining

The confluence of rising oil prices, geopolitical instability, and supply chain vulnerabilities presents a complex challenge for the global mining industry. While individual mines may have tailored strategies to mitigate immediate impacts, the long-term trend suggests a reinforcement of the industry’s inherent vulnerability to disruptions in global fuel markets.

Sustained energy price increases have the potential to:

- Reshape Industry Cost Curves: Assets with higher operating costs, particularly those heavily reliant on fossil fuels and located in regions with less access to affordable energy, may become less competitive. This could lead to shifts in production and investment priorities.

- Impact Project Economics: The viability of new mining projects, especially those with long lead times and significant upfront capital investment, will be more heavily scrutinized in light of uncertain future energy costs. This could slow down exploration and development.

- Accelerate the Energy Transition: Paradoxically, the increased cost and volatility of fossil fuels may serve as a powerful catalyst for the mining industry to accelerate its own transition towards renewable energy sources and more sustainable operational practices. Companies that can demonstrate greater energy independence and resilience will likely gain a competitive advantage.

In conclusion, the current geopolitical climate in the Middle East and its impact on oil prices represent a significant headwind for the mining sector. The BMO Capital Markets report provides crucial data and analysis, illustrating that the effects extend far beyond direct fuel costs, permeating the entire value chain. As the industry navigates these turbulent times, strategic investments in energy efficiency, diversification of energy sources, and robust supply chain management will be paramount to maintaining profitability and ensuring the continued responsible extraction of essential mineral resources. The lessons learned from this period of heightened volatility will undoubtedly shape the future operational strategies and investment decisions of mining companies worldwide.